The core of "deep learning" in artificial intelligence (AI) is increasingly being integrated into the automotive supply chain, alongside advancements in 5G and lithium battery charging technologies. Fubon Securities believes that the future of the automobile industry will be defined by three major trends: automation (Autonomous), connectivity (Connected), and electrification (Electrified). These trends are creating significant business opportunities for Taiwan's technology manufacturers.

The Consumer Electronics Show (CES) held in Las Vegas each January serves as a key indicator of technological trends. In recent years, major IT companies and automakers have focused on new energy vehicles, car networking applications, and autonomous driving technologies, making them central themes at CES. In fact, CES has even taken on another unofficial name: the Car Electronics Show. As the automotive industry shifts from traditional machinery to high-tech sectors, it presents substantial growth opportunities for Taiwan’s electronics industry.

When examining the development of autonomous driving software and hardware, technologies such as deep learning, visual recognition, and detailed road mapping systems are still in early stages. Moreover, legal and insurance frameworks are not yet fully established. Experts estimate that Level 5 fully autonomous vehicles—capable of operating under all road and weather conditions—will not begin entering the market until 2028. Before that, Advanced Driver Assistance Systems (ADAS) and connected cars will play a critical role in building the sensory and communication systems necessary for full autonomy.

Electric vehicles are also set to become a dominant trend due to government policies promoting energy conservation and carbon reduction. Countries like the Netherlands and Norway plan to ban internal combustion engine vehicles by 2025, with Germany, the UK, and France following suit between 2030 and 2040. This regulatory shift is pushing traditional automakers to invest heavily in electric vehicle development. Compared to conventional gasoline-powered cars, electric vehicles rely on a wide range of electronic components, accelerating the transformation of vehicles into intelligent and connected platforms. Tesla is a prime example of this shift.

In short, the future of the automobile will be driven by three main forces: AI, car networking, and electrification. These changes will significantly reshape both the automotive supply chain and the vehicles themselves. According to research institutions, the annual sales of Level 2 and above electric self-driving vehicles in the U.S., Europe, and China are expected to reach 81 million units by 2030, gradually replacing traditional fuel-powered cars.

Fubon Securities highlights that China’s tech industry has experienced rapid growth in recent years, with electric self-driving vehicles becoming a top priority. According to its "Smart Vehicle Innovation Development Strategy" draft, the goal is to achieve 50% of new smart vehicles by 2020, and to become a global leader in smart vehicles by 2035. A PwC report also predicts that mainland China will surpass the U.S. and Europe to become the largest market for electric self-driving cars by 2030. Clearly, strong policy support and a vast domestic market are key advantages for China’s development in this field.

Indeed, Chinese tech giants are actively investing in the development of electric self-driving vehicles. Baidu has launched the Apollo 2.0 platform, involving over 90 international technology companies. Meanwhile, Tencent and Alibaba are also engaging in car factory collaborations and investments in electric vehicles and car networking. Additionally, emerging Chinese startups like NIO and XPeng have gained attention for their performance at events like CES. It is clear that China’s influence in the electric self-driving car market is growing rapidly.

Car Networking Components Benefit

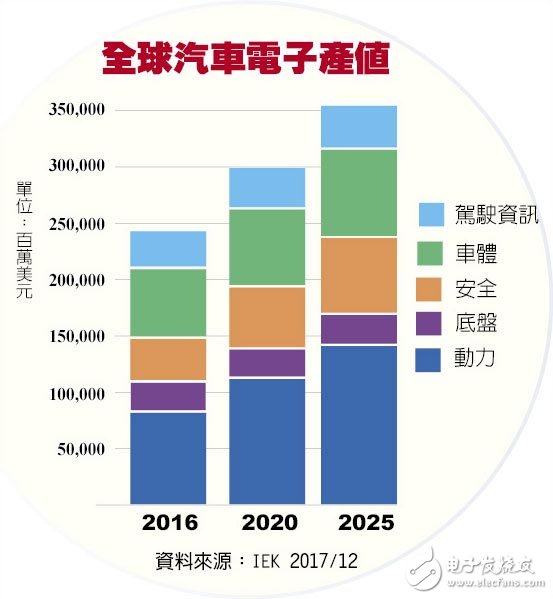

According to the IEK report, the current global automotive electronics production value is around $250 billion. With the ongoing trends of automation, electrification, and connectivity, the industry is expected to exceed $350 billion by 2025. This growth will bring significant business opportunities for Taiwan’s semiconductor and electronic component manufacturers.

Fubon Securities notes that the key components of electric self-driving vehicles can be categorized into four major systems: drive, power, sensing, and control. The first two form the core of the electric self-driving power system, while the latter two are essential for achieving intelligent and even driverless operation.

First, the drive system consists of an electric motor, transmission system, and related controllers. This sector represents a large portion of the motor industry. Second, the power system includes batteries, power modules, power management systems, and charging devices. As the automotive industry moves toward electrification and advanced power systems, vehicle voltage levels are shifting from 12V to 48V, which will lead to changes in electronic power components. This shift is expected to provide long-term benefits for power components such as MOSFETs and IGBTs.

Finally, the "sensing and control system" includes vehicle processors, AI computing chips, memory, sensors, and vehicle networking devices. Vehicle processors must have high-performance computing capabilities to process data from various sensors and perform deep learning for route planning. Sensors use different types of technology—such as ultrasonic, image lenses, radar, and LiDAR—to monitor and control vehicle functions, collect environmental data for ADAS systems, and enhance driver awareness through warnings or automated responses.

Electronic Technology Industry Finds New Blue Sea

Fubon Securities states that the automobile industry, which has been around for over a century, has long operated within a large and closed ecosystem. However, with the entry of tech companies like Google, NVIDIA, Intel, and Tesla, the industry is undergoing a transformation. This shift has created new opportunities for technology electronics manufacturers. Taiwanese electronics firms have been focusing on the automotive electronics market for many years and are now beginning to see tangible results.

According to the Industrial Technology Research Institute, the output value of Taiwan’s automotive electronics is expected to exceed 220 billion NT dollars this year, with a target of 276 billion NT dollars in 2020. This growth rate is faster than the global industry average. Investors are advised to focus on car-electricity groups already in Tesla’s supply chain, as well as IC, sensor, and power component stocks showing strong growth potential.

Solar Pv Test Equipment,Photovoltaic Testing Tools,Solar Iv Tester,Solar Pv Testing Kit

Sowell Electric CO., LTD. , https://www.sowellsolar.com