In the information society, flat-panel display is everywhere. Whether it is TV, computer, smart phone, wearable device, etc., it is inseparable from the support of the display screen. The flat-panel display industry has thus become a “pillar industry†in the field of electronic information.

As a global consumer electronics manufacturing country, China's "lack of core and less screen" was once a major bottleneck restricting the development of related industries in China. In recent years, China has continuously increased investment in the flat panel display industry. At the same time, the government has also introduced a series of industrial support policies to promote the pace of panel localization.

In October 2014, the National Development and Reform Commission and the Ministry of Industry and Information Technology jointly issued the 2014-2016 new display industry innovation development action plan, clearly proposing that by 2016, China's new display industry will strive to reach the second place in the world according to the area. The global market share exceeds 20%, and the overall scale of the industry exceeds 300 billion yuan.

The flat panel display industry has become one of the emerging industries that the country is strongly advocating. Because the display panel is in the middle of the industrial chain, it has the role of supporting the industry chain, which can drive the development of pillar industries such as raw materials, equipment manufacturing and electronic information. Therefore, it will occupy an important position in China's national economy. In May 2016, the state introduced China Manufacturing 2025, which required a shift from a manufacturing power to a manufacturing power, and it will also bring more development momentum to the emerging display industry.

On June 1, 2015, the China-South Korea Free Trade Agreement (FTA) was formally signed, and more than 90% of the products of both parties will enter the era of zero tariff. Among them, in order to alleviate the impact of Korean imported panels on the domestic panel industry, the relevant provisions stipulate that the panel industry tariffs will adopt the “8+2†strategy, that is, after the agreement takes effect, there will be a “protection period†of up to 8 years, maintaining the current 5 The tariff is reduced to 2.5% until the 9th year, and it is reduced to zero tariff in the 10th year.

The eight-year tariff protection period has maximized the time to reduce tariffs, leaving domestic panel makers with sufficient development time. Domestic panel companies will also make full use of this time window to enhance their market competitiveness. From the national promulgation of the 2014-2016 new display industry innovation development action plan to the relevant panel provisions of the China-South Korea FTA, it can be seen that the state is fully promoting the development of the domestic display panel industry at the policy level.

AMOLED market development prospectsIn the global display field, the traditional TFT-LCD-based flat panel display industry has entered a mature stage. In recent years, Korean, Chinese, and Japanese companies have begun to compete to increase the investment layout of the "next-generation display technology" AMOLED in order to seize the new display. The right to speak.

According to the “In-depth Research and Investment Prospect Forecast Report of Intelligent Display Industry 2017-2021†released by China Investment Consulting, AMOLED can provide more realistic image quality, thinner size and more powerful outdoor experience than traditional LCD panels. It has more advantages in eye protection. In the future, the development of flexible AMOLED display technology will further remove the mobile terminal, so it is also regarded as the first choice for smart mobile device panels.

In 2014, the global shipment of AMOLED-equipped smartphones was 200 million, and in 2015 it increased by 23.3% to 250 million. It is estimated that by 2020, the annual compound growth rate of AMOLED panel demand will reach 40.7%.

In addition to smartphones, AMOLED panels have gradually penetrated into smart phones, in-vehicle displays and virtual reality (VR) devices. In 2015, Apple's smart watches and Huawei smart watches have adopted AMOLED displays, and Samsung, Sony, and Oculus' virtual reality devices have also adopted AMOLED panels. It is predicted that there will be more consumer electronics terminal products using AMOLED panels in the future.

AMOLED has triggered a new round of panel technology upgrade competition in the world. At present, in China, panel companies led by Hehui Optoelectronics, Visionox, BOE, etc. are increasing their investment in AMOLED. The first domestic enterprise to achieve medium and small-sized AMOLED mass production and Huiguang announced that it has successfully lit the first 2.6-inch WQHD ultra-high-resolution flexible AMOLED display in China. In early 2015, Visionox announced that its 5.5-generation AMOLED production line in Kunshan entered the trial production phase.

The turning point of the AMOLED industry has already arrived, and it is a good period from the gestation period to the outbreak period. The wave of intelligence has promoted the rapid development of small and medium-sized displays, and AMOLED has gradually replaced the trend in the flagship mobile phone market, smart wear, and virtual reality. Especially in the flagship smartphone field, it has been monopolized by Japanese and Korean companies before, and the market share of Chinese panel companies is zero. The breakthroughs of Chinese companies in this field have, to a certain extent, also broken the long-term monopoly of Japanese and Korean companies.

According to estimates, the domestic display industry will surpass South Korea in 2018, ranking first in the world. In 2014, the total output value of domestic AMOLED exceeded 100 billion, but only 10% of the world. This also means that Chinese panel companies still have considerable room for growth in the global competition.

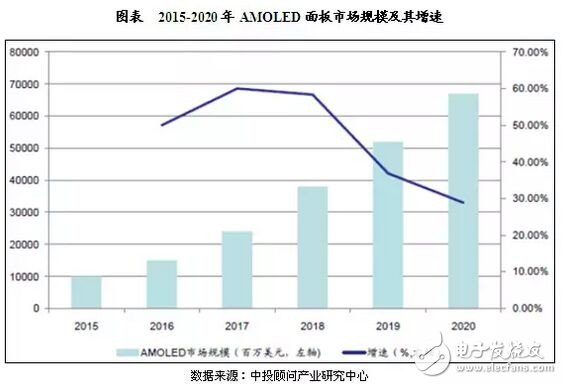

AMOLED market space forecastSubject to capacity constraints, AMOLED screens may see a supply shortage in 2017. According to the "2017-2021 Intelligent Display Industry In-depth Research and Investment Prospect Forecast Report" released by China Investment Consulting, from 2015 to 2016, global OLED products accounted for about 12% to 17% of display product revenue, to 2020. The year is expected to reach 46%. However, the current AMOLED screens in the global market are mainly supplied by Samsung. At present, the annual production capacity of Samsung's OLED screens is around 200 million, and the production capacity is still tight. It is estimated that the average compound growth rate of the industry's output value in the next five years will be around 46%. The AMOLED panel market is expected to reach $15 billion in 2016, an increase of approximately 50% from $10 billion in 2015. By the end of 2020, the AMOLED market will reach US$67 billion, with a compound annual growth rate of approximately 46%.

Lszh Wire,Lszh Grounding Wire,Lsoh Grounding Wire,Lshf Grounding Wire

Baosheng Science&Technology Innovation Co.,Ltd , https://www.bscables.com