The boom in smartphone mobile payment in 2016 has made the NFC market booming. From Apple Pay to China, the full-end mobile phone bus card has blossomed to Huawei inSE and Qualcomm to acquire NXP. These big events are subverting the domestic NFC industry. What is the future NFC market? What challenges does NFC face?

NFC market sizeResearch and Markets released the "2024 NFC Market Analysis Forecast" report this month. The report predicts that the global NFC market will reach $47.43 billion in 2024.

The report pointed out that due to the popularity of smartphones in developing countries, the industry will achieve substantial growth during the forecast period. Research shows that the popularity of mobile payment services will drive the growth of point-of-sale (POS) devices. Bank entities, payment gateways are expected to promote the popularity of new technologies. The report adds that the emergence of mobile wallet services will allow users to pay through mobile devices or through non-cash payment models, which will further drive the growth of the NFC market. As an important part of the Internet of Things, the emergence of wearable technology will also drive industry growth.

The emergence of mobile wallets (such as Android Pay, Apple Pay and Samsung Pay) will further drive the growth of mobile payments. The growing number of suppliers will also drive the development of NFC infrastructure, thereby accelerating market growth.

In addition, the latest research report of TrendForce's Tuoba Industrial Research Institute pointed out that in 2016, smart phone operators continued to build their own payment ecosystem, and various types of payment methods also flourished. This has boosted the global mobile payment business, which estimates that the global mobile payment market will reach $780 billion in 2017, with an annual growth rate of 25.8%.

Xie Yushan, senior research manager of Tuoba, said that in 2016, mobile operators continued to promote their own mobile payment services, of which Apple and Samsung have an absolute advantage. In terms of operating system, since Android (Android) has more than 50% of the global market share, Google In order to expand business opportunities, it also accelerated the internationalization of Android Pay. In December 2016, it announced cooperation with Lotte Japan.

Observing the mobile payment security technology in 2017, Xie Yushan said that in addition to integrating the encryption chip, through the application of encryption algorithm and multi-factor authentication, the identification efficiency of the customer can be improved to obtain relevant authorization and increase the security of data transmission.

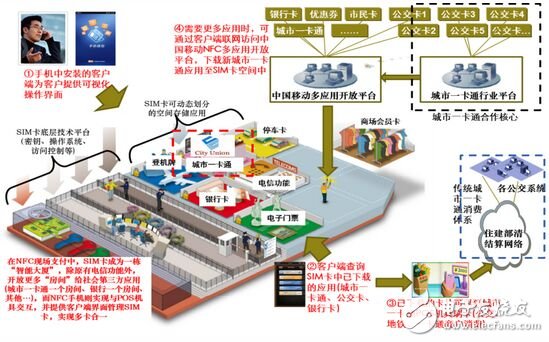

Mobile payment industry chainThe composition of the mobile payment industry chain

Mobile payment is a complex system involving mobile operators, payment service providers, application providers, equipment providers, financial institutions, merchants and consumers. The combination of various factors and collaborative relationships constitute the mobile payment industry. Value Chain. The competitive relationship among the members of the mobile payment industry chain determines the complexity and variability of the mobile payment industry chain. It mainly participates in the difference in the ability of the entity to control key resources such as customers, merchants, accounts, payment channels and payment terminals, resulting in the benefits of the industry chain. Different distribution principles and partnerships result in different business models for mobile payments.

The operation mode of the mobile payment industry chain

With the rapid development of the mobile payment industry, NFC payment applications have once again received attention. In order to gain greater voice and interest in the future industry, the parties have fierce competition for the dominant role in the NFC industry chain. At present, the competition for the dominant role of the domestic NFC industry mainly includes the SWP-SIM solution with mobile operators as the main body, the SWP-SD solution with the bank as the main operation, and the fully-embedded (Embeded SE) solution with the mobile phone manufacturers as the main operators. The main mode of cooperation between the main parties is to collect equipment and technology license fees for the rented card space.

Take the mobile SWP-SIM scheme as an example

The unfavorable factors of NFC landing in the industrial chain and terminal consumptionIndustry chain

The upstream of NFC technology is composed of complex chip suppliers. When this technology is added, the production cost of mobile phone manufacturers will increase;

In addition to upstream chip suppliers, mobile phone manufacturers must simultaneously integrate multiple collaborations between UnionPay, merchants and mobile phone consumers. The industry chain is too long. Since 4G, mobile phone prices have been lower and lower, hardware costs are on the verge of risk, and other Uncertain links, greater risks, and more difficult to control costs;

UnionPay is required to provide terminal payment equipment support, and UnionPay needs to increase investment of about 500 yuan per POS terminal, which takes up a large amount of capital;

In view of the above various risks and costs, NFC technology can only be diluted if it is applied to medium and high-end mobile phones. Apple and Samsung have a considerable sales volume, which is an important way to promote NFC technology, but its cooperation in UnionPay and online shopping platforms has stagnated. For domestic mainstream brands, only Huawei has the ability and appeal to add this feature to its high-end mobile phones, but it does not have the need to act as a multi-industry chain for integrated payments.

End consumer

Android users use NFC to pay, users need to change cards, change phones, in the process of changing cards, users have to bear the risk of privacy leakage, the various information in the card can be copied away at any time, users are worried ;

Compared with the bus card that only needs to pay a deposit of 20 yuan, the cost of changing the machine for thousands of dollars is only for the NFC payment function, which is more difficult for consumers to accept;

It takes time and effort to change cards, and there are not many models that support NFC. There are few options, and the business hall that can change cards is limited. It takes only one minute to apply for a bus card.

In addition to the risk of information leakage, it has been developed for more than ten years, the technology is solidified, the threshold is low, and there are security risks of theft. As long as the card reader can easily interact, the user may be repeatedly brushed without knowing it. Take the balance;

NFC technology requires the signal transmitting end and the receiving end to be used at the same time, and can only be operated at a close distance to realize payment, and has requirements for environment, time, physical distance, and operating posture. Other mainstream payment methods do not have this limitation. For example, if you scan the QR code, you can use the camera and scan code application on the mobile phone, no matter which medium the QR code is printed on, you can read it effectively.

Due to the strong investment and popularization of QR code scanning code payment in the past three years, users have formed operational habits, and their acceptance and usage rate are stable.

NFC technology has too many restrictions on terminals and scenarios, and consumers have to pay a lot of cost if they use this technology, which should be the biggest obstacle to their popularity.

NFC technology can't reach online payment, but the current offline payment method is still based on network support and needs to be completed online. In the near-field payment scenario, NFC has the advantage of offline payment. If you want to popularize, you should find killer application scenarios, such as extensive application on bus cards and bank cards, and establish cooperation with public transportation, subway, UnionPay and merchants.

Reduce the difficulty and risk of using NFC technology and change the way of using NFC. If you put a mobile phone with NFC technology on an ATM, you can start operating related financial services instead of directly by swiping your mobile phone. The safety and near-field timeliness of NFC technology can be maximized and applied.

Flat plate Solar Water Heater is suitable for residential or commercial solar water heating projects.

The titanium coated aluminium absorber sheet absorbs up to 95% of available sunlight converting into usable heat for hot water production. Flat plate solar water heater can supply hot water with temperature between 50 to 60C for household and commercial application.

Flat Plate Solar Water Heater,Flat Plate Collector Solar Water Heater,Flat Panel Solar Water Heater,Flat Plate Water Heater

Linuo Ritter International Co.,Ltd , https://www.lnrtsolarenergy.com